This time of the year, we tend to see more fraud attempts and suspicious activity online and at shopping venues. Use this checklist to keep your finances free from fraudulent activity during the holiday season. #1 Track your transactions Regularly monitor your transaction history in your checking account. Also, keep an eye on your FICO credit report and score on the three major credit reporting bureaus--Experian, TransUnion, and Equifax. Note any suspicious or erroneous activity and contact the bureaus to put a hold on your personal credit until the issue is resolved. #2 Turn on your bank account alerts In your bank account settings, navigate to your account settings to activate account alerts. Typically, you can enable alerts for debit card transactions, payments, ATM withdrawals and deposits, and other types of activity. Remember to set alerts for your credit card accounts as well. #3 Keep your account information to yourself Don't share your bank account passwords with anyone. Use multi-factor authentication (MFA) codes for extra security. Financial institutions and creditors will never ask for your sign-in credentials over the phone. #4 Protect your passwords Regularly update your passwords and make sure they're strong and comply with your bank's password rules. Use a combination of letters, cases, numbers, and special characters. Do not use the same password across different accounts. Try using a password manager to store your passwords if you tend to forget them. Using these tips will help protect your identity and prevent you from becoming a victim of fraud during the holiday season and potentially keep you from losing hundreds or even thousands of dollars.

To learn how to save even more money, sign up for your FREE 15-minute financial consultation with Higher Goals Learning or begin right away Budgeting for a Better Future. Let's face it. We can spend a boat load of money on self care -- including nailcare, haircare, and skincare. Investing in our appearance can cost thousands of dollars a year, and can also bust our budgets. Here are three ways you can be kind to your budget and pamper yourself at the same time. 1. Extend Your Mani and Pedi According to StyleSeat, the average cost of a standard mani pedi which includes filing, cuticle trim, and color is around $60. When you add designs, acrylics, and gel styles, you're into the hundreds. To make your manicure last longer, consider a full gel set. The benefits are a glossier coat, sturdier nails, and no-chip polish. Gel-set nails will cost you $20 to $25 dollars more, but you'll be able to extend the time until your next visit by about two weeks and save some money until the next month. 2. Choose Hair Health Over Hairstyle Some of the latest hair trends can cause damage and ultimately cost more to repair than maintaining a healthy hair regimen in the first place. Try not to blow your budget and ruin your hair by using quality products and consulting with a caring hair stylist. Licensed cosmetologist Jay Lovelace of Lovelylaced Hair and Beauty in Owings Mills, Maryland believes in "healthy hair from start to finish." Her number one rule when it comes to hair care is having a healthy foundation, whether it's a treatment, trim, or taking a break from certain products and styles until the hair is repaired. So, stop ruining your hair and budget and connect with a qualified cosmetologist like Jay. You can contact her at [email protected] or visit lovelylacedhair.com for a consultation. 3. Keep Skincare Simple When great skin is not in our DNA, simple, daily, inexpensive skincare habits can save the day and some cash. Moisturizing and protecting your skin doesn't have to cost an arm and a leg. A basic skincare routine consists of cleansing, toning, and moisturizing. Natural products are typically less costly than commercially produced products and tend to be better for your skin in the long run. Cleansing is simply washing your face. A common natural skin cleanser is a bar of African black soap. A one-pound bar costs about $10 and will usually last for several months with daily use. You can also cleanse your face with DIY mixtures consisting of items you probably already have at home, such as honey and Aloe Vera gel. You can find natural skincare recipes with videos of how to make and apply them online. Final TakeTo maintain your million-dollar look on a budget, all you need to do is cut back on what you spend on nailcare, haircare, haircare, and skincare. In 20 or 30 years, your retirement fund and your mirror will thank you!

For more money-saving strategies, contact me at kathy@highergoalslearning to get started achieving your personal finance goals today.  Traveling is one of my all-time favorite things to do. Seeing new places, meeting new people, and experiencing things I've never done before really excites me. If you also love to travel, you may have noticed how prices have increased on just about everything related to relaxing and enjoying yourself away from home. Advanced planning is key to getting the deals you want and still feel like you've indulgenced yourself with a well-deserved vacation. Here are five money-saving travel tips to consider. 1. Eat Local CuisineIf you enjoy visiting culinary hotspots like Morocco, Mexico, and Thailand, you know that dining out can quickly become expensive. Explore local markets, food trucks, and street food vendors to experience delicious authentic cuisine at a fraction of the cost of restaurant dining. 2. Find Travel Packages and DealsLook for travel packages and deals that bundle flights, accommodations, attractions, and excursions. Online travel sites like Expedia and TripAdvisor offer discounted packages and promotions. Be sure to sign into your account for even better deals. Most of the time, when you book a travel package, you save more compared to booking the components separately. 3. Ditch the HotelsInstead of booking a one-room hotel, explore alternative accommodation options like an Airbnb or large guest house if you're traveling with a group. These options can be more cost effective. In more rural areas, consider staying at a camping site or a local bed and breakfast for a more authentic experience. 4. Do a Destination SwapLook for less expensive options to popular tourist spots. These destinations also tend to be less crowded. For example, instead of trekking to Outer Banks, North Carolina, consider Crystal Coast, North Carolina just 85 miles south. Both locations offer fishing, coastal tranquility, and diving. For an international swap, instead of the beautiful South of France, opt for just-as-quaint Newport, Rhode Island in New England, U.S. You'll enjoy sailing, seafood, and wine tasting without breaking the bank. 5. Travel Off-PeakTo significantly reduce costs, plan to travel during off-peak seasons. Sought-after tourist destinations often have lower prices when demand is low, such as when schools are in session. You'll take advantage of lower prices on flights, accommodations, and activities. Remember to plan ahead and book in advance, compare prices across multiple travel sites, and be as flexible as your schedule allows to find travel dates with the best deals. Use these tips to help you plan and enjoy a memorable vacation without straining your budget. Mastering Your Money: A Monthly Guide to Financial Wellness Do you know the tasks you need to do each month to make sure you're in the best financial shape throughout the year? Learn how to prepare for when your financial situation changes. Prevent stressing about money and develop a systematic plan to manage your entire financial health.

Join Higher Goals Learning on Saturday, April 20, 2024 at 12:00 p.m. EDT for a two-hour impactful online workshop for instructions and discussion to automate your financial plan. You'll learn how to decrease your monthly expenses by reviewing your account statements, ways to increase your income and savings, what to do financially on "milestone" birthdays, and much more! Sign up now to get your seat. You can't afford to miss it. You'll also receive a FREE Personal Finance Calendar template to customize with your individual regular monthly financial tasks and birthday and life events.  Living a simple, frugal life looks different from person to person. Your preferences and goals ultimately determine how you live. Don't feel like you can't ever spend any money while cutting back on your lifestyle.

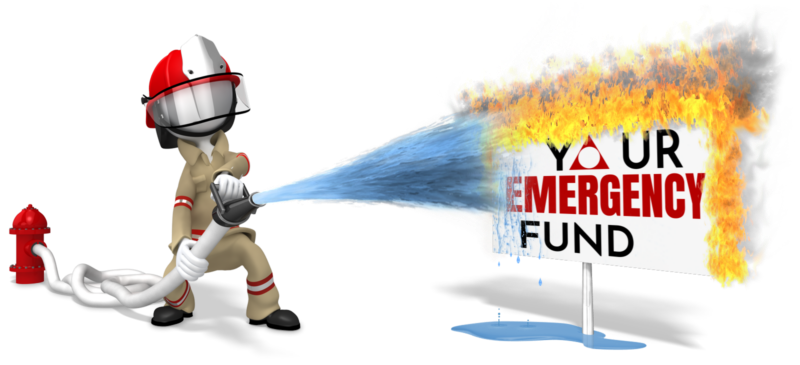

These frugal living tips can help you enjoy life while managing your money and saving some along the way. 1. Travel Economically Vacations are definitely still an option even when you're living a frugal life. If you value travel, you can curb your spending in other areas. Frugal travel planning may take some creativity. Instead of booking expensive hotel suites, use other accommodation options like Airbnb or Vrbo. Instead of hopping on a plane, choose destinations that you can drive to. Road trips can be fun, and you can pack your food instead of stopping at restaurants. 2. Cook Your Meals At Home Dining out can be costly. Save on food costs by cooking in more than eating out. If your culinary skills are challenged, the internet is your friend. Search any food item, and tons of recipes and videos will show you how to cook simple, expensive meals. Most people overspend in the area of food because they lack time. However, there are many meals that you can prepare in under 30 minutes. Meal planning (batch cooking) once a week can also keep you out of the kitchen every night. 3. Borrow Or Shop Used For things you really need or want, see if you can buy them used first instead of purchasing the items new. Thrift store shopping has become all the rage, as well as social media marketplaces. If you need to buy textbooks for school, you can even borrow or rent them instead of buying them new. Buying used and borrowing can save you thousands of dollars that you can put toward other financial goals. 4. Reduce Entertainment Costs You can enjoy some of your favorite entertainment activities at low or no cost. If you use a credit card that offers rewards, save up your points and use them to book your next vacation flight or take your significant other out for dinner at a fancy restaurant. If you're a sports fan, check out a high school game instead of splurging on a professional sporting event. 5. Monetize Your Hobbies What are your hobbies? If you're a singer, musician, craftsperson, or have other talents, why not make some money doing what you love? Tap into your side hustler nature and earn money without feeling like it's work. Use the extra cash to pay off debt while you continue living frugally. Frugality isn't about being cheap. The purpose of living frugally is to allow you to spend your money on the things you value the most. You not only save money, but you gain more control of your life. To optimize the money you have to meet your goals and stay within your budget, consider frugal living.  Saving money doesn't just happen. You have to plan for it and be intentional about it. If you find that you consistently don't have money left over at the end of the month, then make a deliberate effort toward savings planning. First, start by assessing your current financial situation, then develop an effective and consistent strategy. Here are five tips to get you started. 1. Adjust Your Temperature Take a look at your winter and summer thermostat settings. Can you turn the heat down even one or two degrees in the winter and up one or two degrees in the summer and still be comfortable? According to the Department of Energy, minor thermostat adjustments can reduce your spending on energy by up to 10% annually. 2. Get Grocery Deals Groceries are expensive, and it seems like we are shopping more frequently during the pandemic. So, how can we save money on our favorite foods at the grocery store? Try using the stores' weekly ads and creating meals around what's on sale. Compare prices at different stores to see which one has the best deals that week. For non-perishable bulk foods, the "big box" stores often have more value for the money. You'll soon find that the more attention you pay to your grocery shopping, the healthier your food choices become. 3. Buy Off-Season After major holidays, many stores have significant savings. If you have room to store them without creating clutter, buy holiday decorations for the next year. You can find significant savings on clothing as the seasons change. The money you save by shopping off-season can be transferred into your savings account. 4. Budget for Your Savings Make a separate line item or budget category for your savings like a regular monthly expense. Consistently depositing money into your savings will leave less room for unnecessary spending and will get you closer to your savings goals. Determine a specific amount that you can save each pay period, week, or month and make it a "payment" to your savings account just as you would any other "bill." 5. Track and Trim Your Spending What are some of the biggest budget busters that are keeping you from saving as much as you can--fast food, streaming services? Have you ever tracked how much you spend on some of these non-essential items? Tracking can be a wake-up call into our spending habits and encourage us to make different choices and some changes. Cutting back on unnecessary spending will help you boost your savings account. No matter which of these savings tips you initiate, it will only be effective if you commit to your savings plan and follow through consistently every week and month. Saving $50 on groceries is great, but you have to put that $50 into savings. Well-planned and consistent savings will create a good habit of money management, building your savings, and lead you on your way to a stable financial future. "Uh, oh. Why is my car making that knocking noise?" Most of us have heard that dreaded, repetitive "thump, thump, thump" at some point or another. You guessed it--a flat tire. Your tire blowout may have even sounded like a gun shot. Of all the times for car trouble to occur, it happens while you are in a hurry to get to work or some other obligation. But, the most troubling thing on your mind is "How am I going to pay for a new tire if this one can't be patched?" Well, I'll tell you how--with your emergency fund!

What is an Emergency Fund, and Why Do You Need One?

An emergency fund is simply money you have set aside in a separate account to pay for those things that happen unexpectedly--you know--emergencies. What exactly constitutes an emergency? It can be anything from auto repairs (remember the tire blow out on your way to work?), to your air conditioner stopping in mid-July, to losing your job and finding yourself unemployed for four months before finding a new one. Unfortunately, most of us need an emergency fund when we are the least financially stable. It takes time to build an emergency fund, and you have to intentionally save for emergencies in your budget. Ideally, you want to avoid using credit to build your emergency fund. Use the cash you have in your savings account to avoid ending up paying a bill higher than the the original cost of the emergency. Some Tips for Building Your Emergency Fund 1. Track your expenses. How much of an emergency fund do you really need? Your spending and saving habits will help you decide. Determine how much money you spend on average per month month. Include household expenses like utilities, car payments, gas, insurance, and food. Multiply your average monthly spending by the number of months you think you'll need in the event of a loss of income. 2. Be consistent. I recommend saving three to six months' of living expenses. It may take you a while to save enough, but be consistent and you will soon reach your goal. Don't be discouraged if the amount you need seems large at first. Consistent budgeting and saving can help you sock away at least one month of expenses in case of an emergency. One month is better than nothing at all. As you get pay raises, income tax refunds, and birthday cash gifts, you can increase the amount of your emergency savings over time. 3. Keep it liquid. Your emergency fund should be saved in an easily accessible bank account, separate from your regular checking and savings accounts. This way, you always know how much you have saved, and you can easily withdraw it when needed. Savings accounts and money market accounts are excellent vehicles for liquid savings. Retirement savings accounts are not suitable as emergency fund accounts. Withdrawing money from retirement funds prematurely can cost you early withdrawal penalties and extra taxes. Using credit cards can cost you finance charges and interest above the cost of emergencies themselves. Find the Money Don't let the fact that you don't have enough money saved up right now for emergencies discourage you. Start tracking every cent this month to see where your money is going and where money is being wasted. If there are expenses that you can cut back on or eliminate completely, then do it. Add your emergency fund as a line item in your budget, giving it priority. If you need help finding the money in your budget to save for emergencies, Higher Goals Learning Online can show you how. Sign up for one of our online personal finance courses, and for one-on-one personal finance budget coaching, set up a session with me here. Start saving and building the emergency fund that's right for you today!  Financial success is possible regardless of your background, upbringing, education level, or socioeconomic status. Obstacles and hardships don't have to permanently hold you back from winning with money. Instead of stagnating you, let these circumstances become tools that guide and motivate you to your financial a destiny.

Women just like you have told countless stories of their journeys from poverty or meager means to financial freedom. Women who have achieved financial success have also encountered and overcome obstacles. They've earned college degrees, become entrepreneurs, investors, and even millionaires. You can do it, too! Money is a powerful tool, and when used wisely, it can create life-enhancing opportunities. What are some obstacles that we can encounter along our journey to financial success? Family, culture, mistakes, and yes...haters. But guess what? Taking care of yourself, your family, and your loved ones requires money. Spending more time with them requires money. Quality education and cultural experiences require money. Having the best of things and the time to enjoy them requires money. So, turn your obstacles on their heads by putting in the work to improve your financial situation. Prepare yourself to take your financial life into your own hands. Let Higher Goals Learning Online help guide you through the process of growing your wealth. Our informative and engaging courses teach women just like you techniques on managing money, no matter how much or how little you earn. Join Higher Goals Learning Online and expand your financial horizon. Conquer your money fears, doubts, and obstacles. Our lessons are simple, easy-to-grasp concepts that show you how to be a super power at financial obstacle slaying! Despite obstacles, you CAN be wealthy in money, time, and life! Take a course today! |

Kathy T. EvansCertified Personal Finance Instructor and Consultant

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed