This time of the year, we tend to see more fraud attempts and suspicious activity online and at shopping venues. Use this checklist to keep your finances free from fraudulent activity during the holiday season. #1 Track your transactions Regularly monitor your transaction history in your checking account. Also, keep an eye on your FICO credit report and score on the three major credit reporting bureaus--Experian, TransUnion, and Equifax. Note any suspicious or erroneous activity and contact the bureaus to put a hold on your personal credit until the issue is resolved. #2 Turn on your bank account alerts In your bank account settings, navigate to your account settings to activate account alerts. Typically, you can enable alerts for debit card transactions, payments, ATM withdrawals and deposits, and other types of activity. Remember to set alerts for your credit card accounts as well. #3 Keep your account information to yourself Don't share your bank account passwords with anyone. Use multi-factor authentication (MFA) codes for extra security. Financial institutions and creditors will never ask for your sign-in credentials over the phone. #4 Protect your passwords Regularly update your passwords and make sure they're strong and comply with your bank's password rules. Use a combination of letters, cases, numbers, and special characters. Do not use the same password across different accounts. Try using a password manager to store your passwords if you tend to forget them. Using these tips will help protect your identity and prevent you from becoming a victim of fraud during the holiday season and potentially keep you from losing hundreds or even thousands of dollars.

To learn how to save even more money, sign up for your FREE 15-minute financial consultation with Higher Goals Learning or begin right away Budgeting for a Better Future. "Uh, oh. Why is my car making that knocking noise?" Most of us have heard that dreaded, repetitive "thump, thump, thump" at some point or another. You guessed it--a flat tire. Your tire blowout may have even sounded like a gun shot. Of all the times for car trouble to occur, it happens while you are in a hurry to get to work or some other obligation. But, the most troubling thing on your mind is "How am I going to pay for a new tire if this one can't be patched?" Well, I'll tell you how--with your emergency fund!

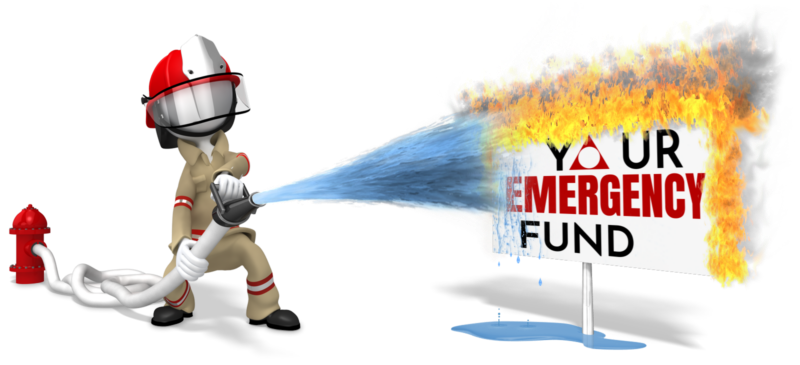

What is an Emergency Fund, and Why Do You Need One?

An emergency fund is simply money you have set aside in a separate account to pay for those things that happen unexpectedly--you know--emergencies. What exactly constitutes an emergency? It can be anything from auto repairs (remember the tire blow out on your way to work?), to your air conditioner stopping in mid-July, to losing your job and finding yourself unemployed for four months before finding a new one. Unfortunately, most of us need an emergency fund when we are the least financially stable. It takes time to build an emergency fund, and you have to intentionally save for emergencies in your budget. Ideally, you want to avoid using credit to build your emergency fund. Use the cash you have in your savings account to avoid ending up paying a bill higher than the the original cost of the emergency. Some Tips for Building Your Emergency Fund 1. Track your expenses. How much of an emergency fund do you really need? Your spending and saving habits will help you decide. Determine how much money you spend on average per month month. Include household expenses like utilities, car payments, gas, insurance, and food. Multiply your average monthly spending by the number of months you think you'll need in the event of a loss of income. 2. Be consistent. I recommend saving three to six months' of living expenses. It may take you a while to save enough, but be consistent and you will soon reach your goal. Don't be discouraged if the amount you need seems large at first. Consistent budgeting and saving can help you sock away at least one month of expenses in case of an emergency. One month is better than nothing at all. As you get pay raises, income tax refunds, and birthday cash gifts, you can increase the amount of your emergency savings over time. 3. Keep it liquid. Your emergency fund should be saved in an easily accessible bank account, separate from your regular checking and savings accounts. This way, you always know how much you have saved, and you can easily withdraw it when needed. Savings accounts and money market accounts are excellent vehicles for liquid savings. Retirement savings accounts are not suitable as emergency fund accounts. Withdrawing money from retirement funds prematurely can cost you early withdrawal penalties and extra taxes. Using credit cards can cost you finance charges and interest above the cost of emergencies themselves. Find the Money Don't let the fact that you don't have enough money saved up right now for emergencies discourage you. Start tracking every cent this month to see where your money is going and where money is being wasted. If there are expenses that you can cut back on or eliminate completely, then do it. Add your emergency fund as a line item in your budget, giving it priority. If you need help finding the money in your budget to save for emergencies, Higher Goals Learning Online can show you how. Sign up for one of our online personal finance courses, and for one-on-one personal finance budget coaching, set up a session with me here. Start saving and building the emergency fund that's right for you today!  Financial success is possible regardless of your background, upbringing, education level, or socioeconomic status. Obstacles and hardships don't have to permanently hold you back from winning with money. Instead of stagnating you, let these circumstances become tools that guide and motivate you to your financial a destiny.

Women just like you have told countless stories of their journeys from poverty or meager means to financial freedom. Women who have achieved financial success have also encountered and overcome obstacles. They've earned college degrees, become entrepreneurs, investors, and even millionaires. You can do it, too! Money is a powerful tool, and when used wisely, it can create life-enhancing opportunities. What are some obstacles that we can encounter along our journey to financial success? Family, culture, mistakes, and yes...haters. But guess what? Taking care of yourself, your family, and your loved ones requires money. Spending more time with them requires money. Quality education and cultural experiences require money. Having the best of things and the time to enjoy them requires money. So, turn your obstacles on their heads by putting in the work to improve your financial situation. Prepare yourself to take your financial life into your own hands. Let Higher Goals Learning Online help guide you through the process of growing your wealth. Our informative and engaging courses teach women just like you techniques on managing money, no matter how much or how little you earn. Join Higher Goals Learning Online and expand your financial horizon. Conquer your money fears, doubts, and obstacles. Our lessons are simple, easy-to-grasp concepts that show you how to be a super power at financial obstacle slaying! Despite obstacles, you CAN be wealthy in money, time, and life! Take a course today! |

Kathy T. EvansCertified Personal Finance Instructor and Consultant

Archives

December 2023

Categories

All

|

RSS Feed

RSS Feed